Federal Tax Authority published long-awaited circular letter on February 11

On 1 February 2022, the new circular letter (hereafter also circular) of the Federal Tax Administration (ESTV) No. 5a came into force, replacing circular letter no. 5, which had been in force since 2004. Like its predecessor, the new circular letter deals with the tax implications at federal level (direct federal tax, withholding tax, stamp duties) of reorganisations of partnerships and legal entities at both company and shareholder levels. Although the circular is not binding for cantonal taxes, it is also applied in principle by the cantons, although some cantons deviate from the circular in their practice. The reason for the comprehensive revision of the circular was the various changes in law and practice that have occurred since its entry into force. Thus, in addition to general editorial changes such as the adaptation of terminology to the new accounting law, the new circular primarily contains legal adaptations to various federal laws as well as the adoption of the current relevant case law. The structure of the previous circular has been retained.

General changes

The new circular takes into account the changes of the Corporate Tax Reform II, such as the reduction of the qualifying participation level from 20 % to 10 % for the participation deduction and the introduction of capital contribution reserves (Kapitaleinlagereserven, KER). Furthermore, the instruments introduced as part of the tax reform/AHV financing (STAF or corporate tax reform III), such as the "immigration step up", are included. The circular also clarifies that the tax neutrality of a restructuring for the emissions levy and turnover tax does not require the transfer of the profit or income tax values and that the civil law structure of the restructuring is irrelevant for tax purposes.

The most significant changes in the new circular are:

- Additional possibility to split a holding company. A holding company that holds more than 50 % of the voting rights in two or more operating companies can spin off one of these companies to a new holding company in a tax-neutral manner;

- Reduction of the participation quota. The circular now confirms that for the tax-neutral transfer of a participation to a subsidiary (sub-holding), a 10 % participation (previously 20 %) in both the transferred participation and the receiving subsidiary is sufficient. A 10 % participation is now also sufficient for the purposes of the replacement of a participation;

- Partial profit tax-neutral restructuring is possible. If, in the course of a restructuring, hidden reserves on individual assets are not transferred in a completely tax-neutral manner by increasing the relevant profit tax values to a value below the market value, only the difference between the profit tax values before and after the restructuring is generally subject to profit tax at the transferring company. The transferred hidden reserves are not taxed;

- No legal basis for levying stamp duty in the event of a blocking period violation. The new circular also confirms the case law that the stamp duty on issues and the stamp duty on turnover do not recognise any blocking periods and therefore a possible blocking period violation in the case of profit taxes does not have any tax consequences in the case of the stamp duty on issues or the stamp duty on turnover. Although, in the case of the stamp duty on issues the possibility of a tax evasion can be examined.

In addition, various detailed adjustments have been made, so that an examination of the new circular before planning and implementing a restructuring is indispensable, even for experienced tax advisors.

The aforementioned significant changes as well as some others changes are discussed in detail below.

Selected changes in detail

1. Merger (Fusion)

a) Increased flexibility in the rules on the assumption of losses - economic approach decisive

As before, in the case of a merger, the untaxed hidden reserves can be transferred to the acquiring company in a tax-neutral manner, provided the tax liability in Switzerland continues to exist cumulatively and the values previously relevant for profit tax are adopted. The acquiring company may claim the previous year's losses of the transferring company not yet taken into account in the calculation of the taxable net profit pursuant to Article 67 paragraph 1 of the Federal Act on Direct Federal Tax (DBG). Now, a previous reorganisation of the acquired companies is explicitly no longer detrimental. A "doubling" of value adjustment on participation and loss transfer is permissible.

A takeover of the previous year's losses was and is excluded if there is tax avoidance. Until now, according to circular letter no. 5, this was always the case in the event of a so-called shell company, i.e. if the transferring company was economically liquidated or if a business transferred by the merger was discontinued shortly after the merger.

Based on existing decisions of the Federal Supreme Court (Bundesgericht), the discontinuation of a business transferred through a merger is no longer automatically classified as tax avoidance in every case. Now, a takeover of the previous year's losses is only excluded if, viewed dynamically, there are no business reasons for a merger. The terminology of a "dynamic consideration" refers to the case law of the Federal Supreme Court and means that business reasons or the intention of the acquiring company to use the acquired assets after the merger are also taken into account. Accordingly, a lack of economic reason exists if the transferring or the acquired company is inactive and therefore no longer uses its assets and the other active company has no benefit whatsoever from these assets (lack of synergies). However, if the other active company can use the acquired assets, e.g. patents or customer lists, for business purposes again, there is no tax avoidance and the takeover of the previous year's losses must be recognised.

b) Offsetting of increases in nominal value with capital contribution reserves possible for income tax purposes

If a natural person experiences an increase in the nominal value of the shares held by him/her as a result of a restructuring, this triggers income and withholding tax consequences to the same extent as before (free increase in nominal value). The tax consequences of a nominal value increase or of compensation payments can still be prevented by offsetting them against nominal value losses. The new circular also confirms the practice of the ESTV that the taxation of an increase in nominal value can also be averted by offsetting against KER. An increase in the proportional KER without an increase in par value is not taxed for the unit holder due to the lack of legal basis.

2. Split

a) Mandatory takeover of previous year's losses

There is a change with regard to the transfer of previous year's losses in the case of demergers. In the case of a demerger, the previous year's losses not yet taken into account in the calculation of the taxable net profit, which are attributable to the transferred business or partial business, must be transferred to the acquiring company. This mandatory provision replaces the optional provision in the old circular. In the case of a transfer of a business, a detailed breakdown of the losses associated with the business must now always be provided. As already mentioned, however, a transfer of the previous year's losses is excluded if there is tax avoidance. In the case of a demerger, this will be examined in particular if the transferred business is discontinued shortly after the demerger. The mandatory loss allocation also applies in the case of a transfer of a business or part of a business to a subsidiary or group company.

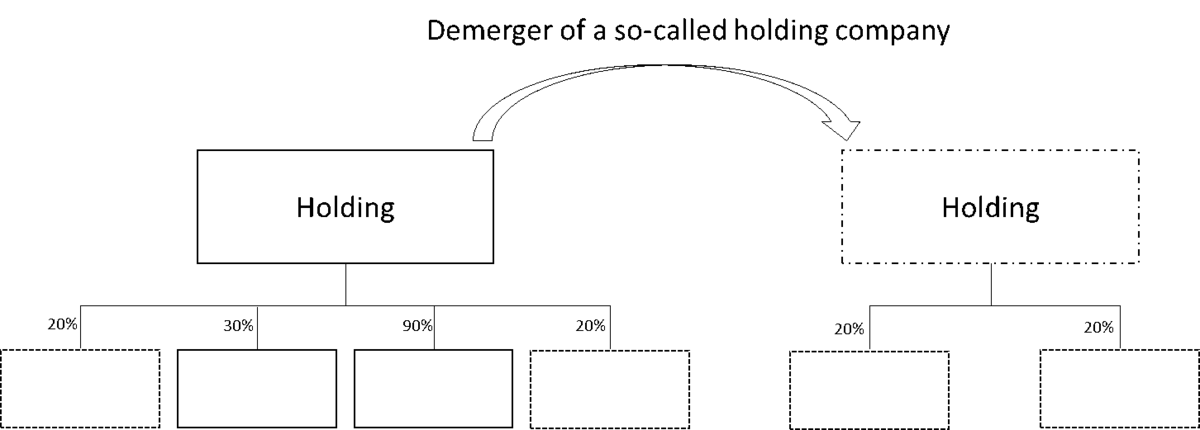

b) Additional possibility to split a holding company

Holding and managing securities that serve only to invest one's own assets never constitutes a business (asset management companies), even if the assets are large, as was previously the case. In contrast, the holding and management of participations may qualify as a business. A tax-neutral holding company split is possible in cases where, from a tax perspective, the operating requirement for the purposes of the restructuring is met both for the spun-off holding structure and for the remaining structure consisting of holding company and subsidiary. As before, the operating requirement can be fulfilled at the holding company. Now, the operating requirement can also be fulfilled at the level of the active company in which the holding company has an interest, in compliance with the so-called transparency principle.

(i) Holding company (existing practice)

A holding company exists if (i) they are mainly operating (active) companies, (ii) the participations account for at least 20 % of the share capital or nominal capital of the other companies or otherwise make it possible to have significant control, (iii) the holding companies existing after the demerger actually perform a holding function (at least two participation of 20 % each) with their own staff or through appointed persons and (iv) the holding activity is continued after the demerger.

Authors: Nadia Tarolli Schmidt, Adrian Briner

(ii) Operational (new practice due to case law)

A tax-neutral demerger of a holding company is also possible according to the new circular if the holding company does not have an actual holding company with staff, but holds a majority of votes (more than 50 %) in two (or more) domestic or foreign active, operating companies (so-called transparency principle). In application of this so-called transparency principle, the transfer or spin-off of one of these participations to the acquiring company is sufficient for both the previous and the new holding company to qualify as an operation at the holding company level (Federal Supreme Court ruling 2C_34/2018 of March 11th 2019).

c) Holding company split - special cases

(i) Tax trap - timely absorption

In the case of a holding company demerger with timely absorption of the new holding company with the new operating subsidiary held by it (within 2-3 years after the demerger), the ESTV assumes, under certain circumstances, a reclassification of the originally tax-neutral holding demerger into a distribution of the participation in the operating company to the shareholder (so called dividend in kind; Naturaldividende).

To the extent of the realised hidden reserves on the participation in the new operating company, the old holding company realises a taxable profit, which, however, is largely relieved by the participation deduction if the one-year holding period is fulfilled. In addition, the dividend in kind is subject to withholding tax at the level of the old holding company. For the shareholder, on the other hand, the dividend represents taxable investment income. This is subject to partial taxation if the shareholding in the old holding company was at least 10 %. If applicable, the taxation takes place in the retro perspective tax assessment (Nachsteuerverfahren).

(ii) Tax-free capital gain despite timely absorption upon sale of the new holding company

However, a demerger of a holding company with timely absorption of the operating company with the new holding company after the sale of the new holding company to a third party is generally harmless. The prerequisite for this is that the seller does not know at the time of the sale that the buyer of the new holding company will carry out an absorption of the operating company (absorption must be uncertain).

3. Transfer to subsidiary (subsidiary spin-off)

a) Spin-off of businesses, parts of businesses and fixed assets of businesses

(i) Further qualifying participation of 20 % required for profit tax-neutral transfer

In a spin-off, a company transfers assets to a subsidiary, i.e. to a company in which it intends to participate or in which it already has an interest. Such a transfer can take place by way of a contribution in kind, a sale or a transfer of assets.

In principle, hidden capital contributions lead to taxation of the hidden reserves transferred to a subsidiary and to a corresponding increase in the profit tax value and the cost price of the participation. The transfer of assets to a subsidiary, however, is possible in a tax-neutral manner in the sense of an exception, provided that five cumulative conditions are met: (i) a continuing tax liability in Switzerland, (ii) a transfer of the profit tax values, (iii) the transfer of a business, part of a business or of fixed assets, (iv) the transfer to a domestic subsidiary and (v) the observance of a holding period of five years, whereby this period relates to the acquiring subsidiary and the assets transferred to it.

In the new circular, the domestic subsidiary must still be a corporation or cooperative with its registered office or effective management in Switzerland, in which the transferring company holds at least 20 % of the share capital. Furthermore, a tax-neutral spin-off can also be made to a Swiss permanent establishment of a foreign subsidiary, provided that it is ensured by means of international tax segregation that the transferred hidden reserves continue to be allocated to Switzerland without restriction. The hopes that a 10 % shareholding would be sufficient were thus not fulfilled.

With regard to the compulsory consideration of previous year's losses, which are attributable to the transferred business or business unit when calculating the taxable net profit, reference is made to the implementation for the demergers (see analogously the explanations under 2. a).

(ii) Breach of blocking period after spin-off does not trigger subsequent issue taxes

The updated circular now states that a violation of the five-year retention period in the case of a spin-off of a business, part of a business or fixed assets of a business no longer results in a subsequent levy of the stamp duty, as there is no legal basis for this. On the other hand, in the case of a quick sale of the acquired assets by the subsidiary, the facts must be examined for possible tax avoidance. However, the tax consequences with regard to taxes on profits, i.e. subsequent taxation of the transferred hidden reserves, must still be taken into account. The clarification regarding the issue tax also applies to asset transfers within the group.

b) Spin-off of participations to a subsidiary

(i) 10 % participation sufficient in the case of a participation spin-off to a subsidiary

In the case of a spin-off of a participation, a company transfers a participation in another company to a domestic or foreign subsidiary. Concerning the tax-neutral spin-off of participations, the new circular confirms the already existing practice that a claim to at least 10 % of the profit and reserves of another company or a participation in the share capital of another company or cooperative is sufficient. However, for the latter qualification the threshold has been lowered so that only a participation of 10% is required compared to the 20% that applied under the old circular letter no.5. This applies to both the transferred participation and the acquiring subsidiary.

As before, the participation in the sub-holding company takes over the profit tax value, the production costs and the holding period of the previously directly held participation. However, the profit tax value and the holding period of the transferred participation are now continued by the acquiring company. The production costs of the transferred participation correspond to the profit tax value. Tax neutrality for stamp duty is not dependent on the transfer of the profit tax values. For example, the transfer of an interest of at least 10 % at fair market value to a subsidiary is taxable for profit tax purposes to the extent of the disclosed hidden reserves, but is exempt from stamp duty, since the necessary conditions for a tax-neutral spin-off are fulfilled. However, in this case the holding period for profit tax starts all over again.

In contrast to the spin-off of businesses, parts of businesses as well as items of business fixed assets, a tax-neutral spin-off of participations is not limited to the transfer to a domestic subsidiary and there is (as before) no lock-up period.

However, the reference that no differentiation is made between subsidiaries and group companies for the turnover tax was deleted in the new circular. The acquisition or sale of taxable deeds in the context of transfers to a domestic or foreign subsidiary of participations of at least 10 % of the share capital or nominal capital of other companies or of participations that entitle the holder to at least 10 % of the profits or reserves of another company is exempt from the turnover tax. However, in the case of a transfer within the group, a minimum participation of 20 % in the transferred shareholding applies for the turnover tax (see following explanations).

4. Transfers between Group companies

a) Transfer between domestic group companies

(i) Tax-neutral transfer of shareholdings of less than 20 % possible, provided there is an indirect shareholding of at least 20 % in the group

In the case of a transfer between domestic group companies, a domestic company transfers assets to another domestic company in which it does not hold an interest. However, one company directly or indirectly controls the transferring and the acquiring company (group). Furthermore, a lock-up period of five years applies for profit tax purposes. If the transferred assets are sold or control is relinquished during the subsequent five years, the transferred hidden reserves are taxed at the level of the transferring company in the retro perspective tax assessment. This retention period also applies to the spin-off of participations to group companies that are not subsidiaries of the transferring group company.

Domestic group companies are companies domiciled or actually managed in Switzerland that are directly or indirectly controlled by a domestic or foreign parent company (majority of voting rights or control by other means).

The transfer of assets to an affiliated domestic group company at profit tax values below the fair market values generally constitutes a hidden profit distribution for the transferring company.

As before, directly held participations of at least 20 % in the share capital or nominal capital of another group company, businesses or parts of businesses, as well as items of business fixed assets can be transferred to other domestic group companies in a tax-neutral manner (Art. 61 para. 3 DBG). The circular now adopts the existing practice of the ESTV, according to which participations of less than 20 % can also be transferred, provided that under the control of a corporation or cooperative there is a direct or indirect participation of at least 20 % in the share capital or nominal capital of this company. Thus, shareholdings of less than 20 % can also be transferred between domestic group companies in a tax-neutral manner. The transfer is also tax-neutral with regard to withholding tax and turnover tax.

As before, it should be noted that a spin-off of participations nevertheless leads to tax consequences if a participation of less than 10 % is transferred to a subsidiary with at least 10 % participation (tax-systematic realisation due to the participation deduction). Likewise, the accounting of the transferred participation at the acquiring subsidiary at a value that is higher than the previous profit tax value at the transferring parent company constitutes a properly taxable revaluation gain and not participation income.

b) Transfer of an interest to a foreign group company

As before, the tax-neutral transfer of a participation to a foreign company requires a participation of at least 20 % of the share capital or nominal capital in another corporation or cooperative. In addition, for withholding tax purposes, a tax-neutral transfer is now only possible to a foreign subsidiary of the transferring domestic parent company (see subsidiary spin-off under 3. B.), but not to a sister company.

(i) Tax-neutral transfer for profit taxes and turnover tax still possible

The transfer of a participation to a foreign group company can continue to be made in a tax-neutral manner, provided that under the control of a domestic corporation or cooperative there is a direct or indirect participation of at least 20 % in the share capital or nominal capital in the transferred company and the acquiring foreign group company is in turn controlled by a domestic group company and thus the transferred hidden reserves remain indirectly resident in Switzerland.

If, however, a participation is transferred to a foreign group company without this being controlled by a domestic group company, the deferred tax burden in Switzerland is cancelled. A tax-neutral transfer is therefore not possible and there is a taxable capital gain in the amount of the realised hidden reserves, which - provided that the requirements are met – results in an entitlement to a entitles to a deduction.

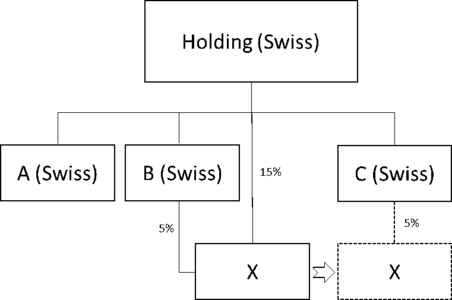

In the case of the turnover tax, a tax-neutral transfer of a shareholding to a foreign group company is also possible, but this requires the transfer of a direct shareholding of at least 20 % in the share capital or nominal capital of another corporation. In contrast to the transfer between domestic group companies, an indirect participation of 20 % is therefore not sufficient for the turnover tax. Thus, in the case example below, a transfer of 20 % is not sufficient, which is why a turnover tax would be due.

(ii) Transfer to foreign group company triggers withholding taxes

The transfer of a participation at the profit tax value to a foreign (sister) group company - regardless of whether this is controlled by another domestic group company - can now no longer be made free of withholding tax. Based on the direct beneficiary theory, the recipient and beneficiary of the refund is the foreign group company receiving the participation (in this case, company B). The application of the reporting procedure is excluded.

Conclusion

The update of circular no. 5 was urgently needed after almost 20 years and two corporate tax reforms. Particularly because the two corporate tax reforms, the introduction of the capital contribution principle and the tightening of the practice of the ESTV with regard to the combination of tax-neutral restructurings, e.g. in the case of timely absorption of a spun-off participation, have made the planning of tax-neutral restructurings more complex in recent years. We therefore welcome the follow-up to earlier practice changes as well as the clarification of various administrative practices in the new circular no. 5a. These lead to legal certainty for the companies. Despite the present circular, an examination of the prerequisites for a tax-neutral restructuring, the planned transaction and the cantonal administrative practice is indispensable in individual cases, especially since the tax assessment is only binding for the tax authorities if a written advance tax ruling has been obtained in advance.

Authors: Nadia Tarolli Schmidt, Adrian Briner

Co-Autor: Jannick Walleser

Nadia Tarolli Schmidt

Attorney at Law, Swiss Certified Tax Expert

- Partner

- +41 58 211 33 54

- [email protected]